$ZETA is approaching a major inflection point.

The company is expected to become profitable as early as next quarter.

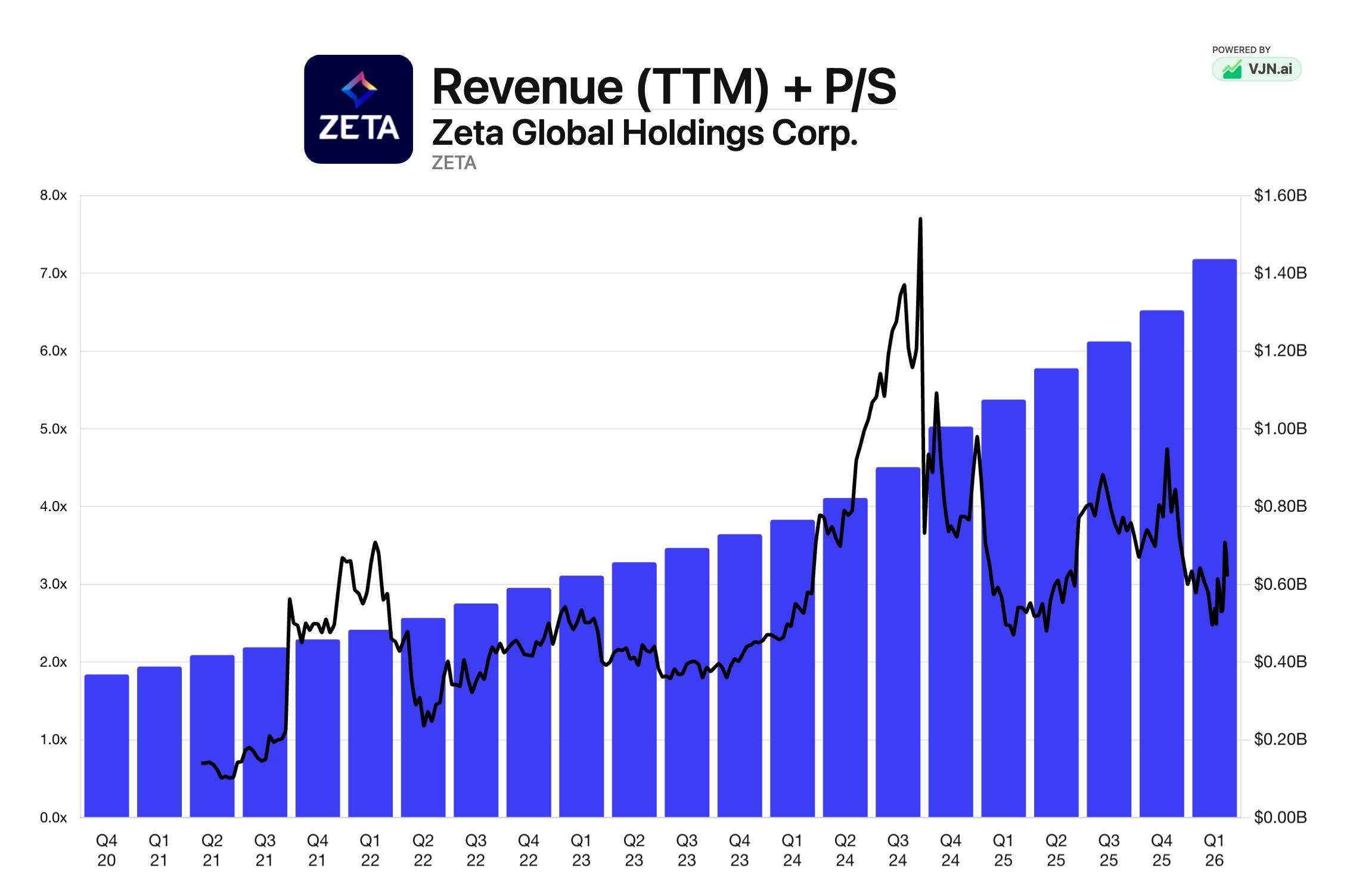

Despite growing revenue at 30%+ annually , the stock is trading at roughly 3x sales .

Looking ahead, current estimates imply a 2027 P/E of just 18x .

At these valuation levels, ZETA doesn’t need exceptionally high margins to look cheap.

If management can sustain growth while reaching profitability, the market may have to reprice the stock significantly higher.

A profitable, 30%+ growth company trading at 3x sales is not something you see every day.