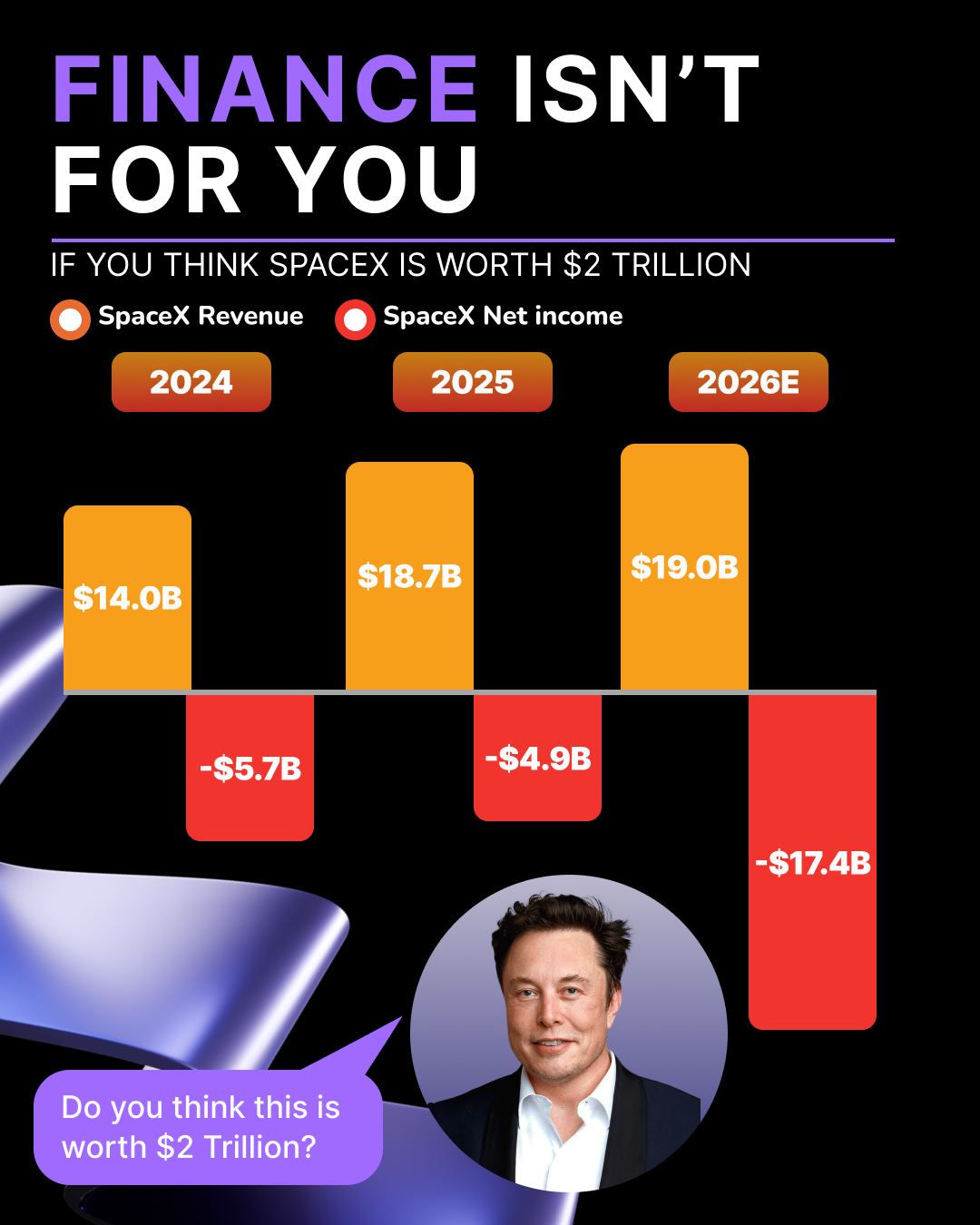

🚀SpaceX: Not a Buy

Is a $1.75T valuation justified? It would be 76x Google’s IPO size and a top-10 global company. Our reverse DCF leaves us unconvinced.

Supporting that price requires roughly 39% annual revenue growth for a decade and ~45% operating margins. No company with $15B+ in revenue has ever sustained such growth, and 45% margins are near-unprecedented for a capital-intensive space hardware business.

🌐The bull case assumes Starlink becomes global communications infrastructure, Starship succeeds commercially, AI/data-center ambitions scale massively, and SpaceX dominates defense, telecom, and logistics. In short, the math only works if SpaceX simultaneously leads several global industries.

Even then, projected returns are ~10% annually-high execution risk for S&P-like performance.