market

Fed Says Basis Trade Key Driver of Hedge Fund Treasury Exposure

Federal Reserve reports hedge funds' Treasury exposure is primarily driven by the revival of the cash-futures basis trade arbitrage strategy.

According to Bloomberg Markets, the Federal Reserve has identified the cash-futures basis trade as the primary driver behind hedge funds' growing exposure to United States Treasury securities. The central bank's assessment, reported on June 24, 2026, highlights the revival of this arbitrage strategy as the key factor shaping hedge fund positioning in the Treasury market. The finding offers insight into how leveraged investors are accessing fixed-income markets and the mechanics behind their increased presence in government debt.

Key takeaways

The Federal Reserve reports that hedge funds' growing Treasury exposure is primarily due to the cash-futures basis trade revival

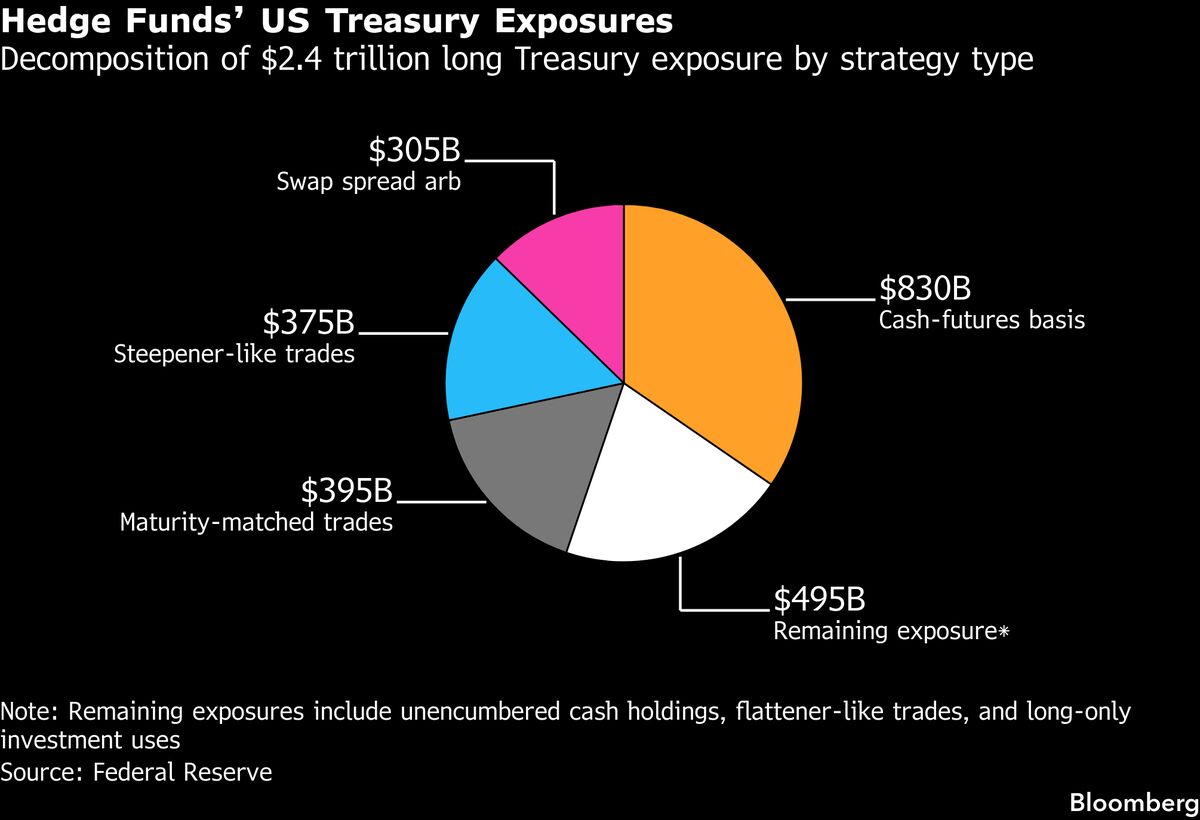

The basis trade is an arbitrage strategy that exploits price differences between cash Treasury securities and Treasury futures contracts

Understanding basis trade mechanics helps explain hedge fund leverage and positioning in fixed-income markets (general context)

Federal Reserve monitoring of basis trades reflects regulatory attention to leverage and systemic risk in Treasury markets (general context)

Table of Contents

What happened

Why it matters

What to watch next

What happened

The Federal Reserve stated that the revival of the cash-futures basis trade is the key driver of hedge funds' growing exposure to Treasury securities. This assessment was reported by Bloomberg Markets on June 24, 2026. The central bank's observation identifies a specific trading strategy as the mechanism through which hedge funds have increased their positions in the government debt market. The basis trade involves simultaneous positions in cash Treasuries and Treasury futures contracts, exploiting pricing discrepancies between the two markets.

The Federal Reserve's identification of this trend suggests the central bank is actively monitoring hedge fund activity in Treasury markets. The statement provides clarity on the composition and motivation behind hedge fund Treasury holdings, distinguishing between directional bets on interest rates and arbitrage strategies designed to capture small pricing inefficiencies. The focus on the basis trade indicates that hedge funds are primarily engaging in relative-value strategies rather than taking outright long or short positions on government debt.

Why it matters

The cash-futures basis trade is a leveraged arbitrage strategy that exploits temporary price differences between physical Treasury securities and Treasury futures contracts. When the futures contract trades at a discount to the theoretical price implied by the cash bond, traders can buy the cash security, sell the futures contract, and lock in a profit by holding the position to delivery. This strategy typically requires significant leverage to generate meaningful returns from small pricing discrepancies, which is why hedge funds with access to repo financing are the primary participants. The trade is considered relatively low-risk when properly hedged, but the leverage involved can amplify losses if positions move against the trader or if financing costs rise unexpectedly.

The Federal Reserve's attention to basis trade activity reflects broader regulatory concerns about leverage and liquidity in Treasury markets. Following the March 2020 Treasury market disruption, when basis trades unwound rapidly and contributed to market stress, regulators have increased monitoring of hedge fund positioning and leverage in fixed-income markets. The basis trade's revival suggests that pricing dislocations have returned to levels that make the strategy attractive, and that hedge funds have rebuilt capacity to deploy capital in these arbitrage opportunities. For market participants, the Federal Reserve's statement signals that policymakers are tracking the size and concentration of these positions as part of financial stability surveillance.

What to watch next

Investors and market observers should monitor Federal Reserve communications for further details on the scale and concentration of basis trade positions among hedge funds. The central bank may provide additional data on Treasury market positioning in its Financial Stability Report or through speeches by Federal Reserve officials. Any indication that basis trade positions have grown to levels that could pose systemic risk would be significant for Treasury market participants, as it could prompt regulatory action or changes to repo market rules. The Federal Reserve's focus on this specific strategy suggests it is a priority area for ongoing surveillance.

Market participants should also watch for changes in the cash-futures basis itself, as widening or narrowing spreads indicate the profitability and sustainability of the trade. A sudden narrowing of the basis could trigger position unwinding, potentially affecting Treasury market liquidity and volatility. Additionally, any shifts in repo financing conditions, such as changes in haircuts or availability of leverage, would directly impact the economics of the basis trade and could lead to adjustments in hedge fund Treasury exposure. The interaction between Federal Reserve policy, Treasury issuance, and hedge fund positioning will remain a key dynamic in fixed-income markets.

Read original source